Ecommerce Payments Explained: A Simple Guide for Online Store Owners

Processing payments is one of the often overlooked parts of running an ecommerce business. Customers expect checkout to be fast, secure, and seamless, but behind every transaction, multiple players are involved: the shopper, the merchant, the payment processor, and both banks.

With global ecommerce revenue projected to reach $3.66 trillion in 2025, choosing the right payment system is more than a technical step. It’s essential for growing your business.

This guide shows you how ecommerce payments work, the main قسط methods, how to choose a processor, and the 5 top providers.

What Are Ecommerce Payments?

Simply put, ecommerce payments are the digital transactions that let customers pay for goods or services online. Most shoppers might think paying online is just a click, but in reality, it’s a carefully managed process that keeps money moving safely and builds trust.

A smooth payment experience can boost conversions, reduce cart abandonment, and encourage repeat purchases, making it a critical part of running any online store.

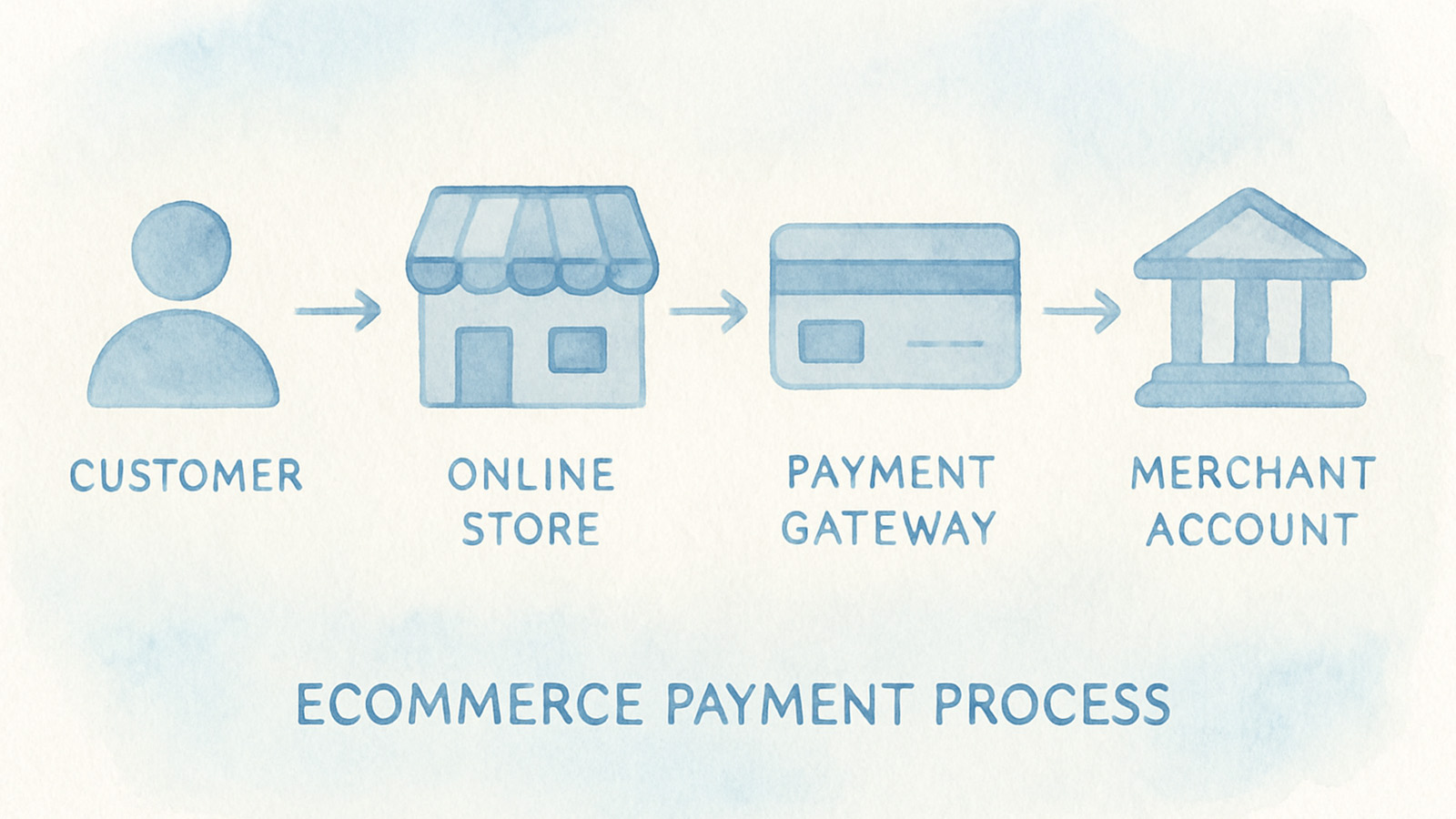

How Ecommerce Payments Processing Works

When someone pays on your online store, several systems work together to verify the payment and move the funds to your business.

Let’s walk through how it actually works.

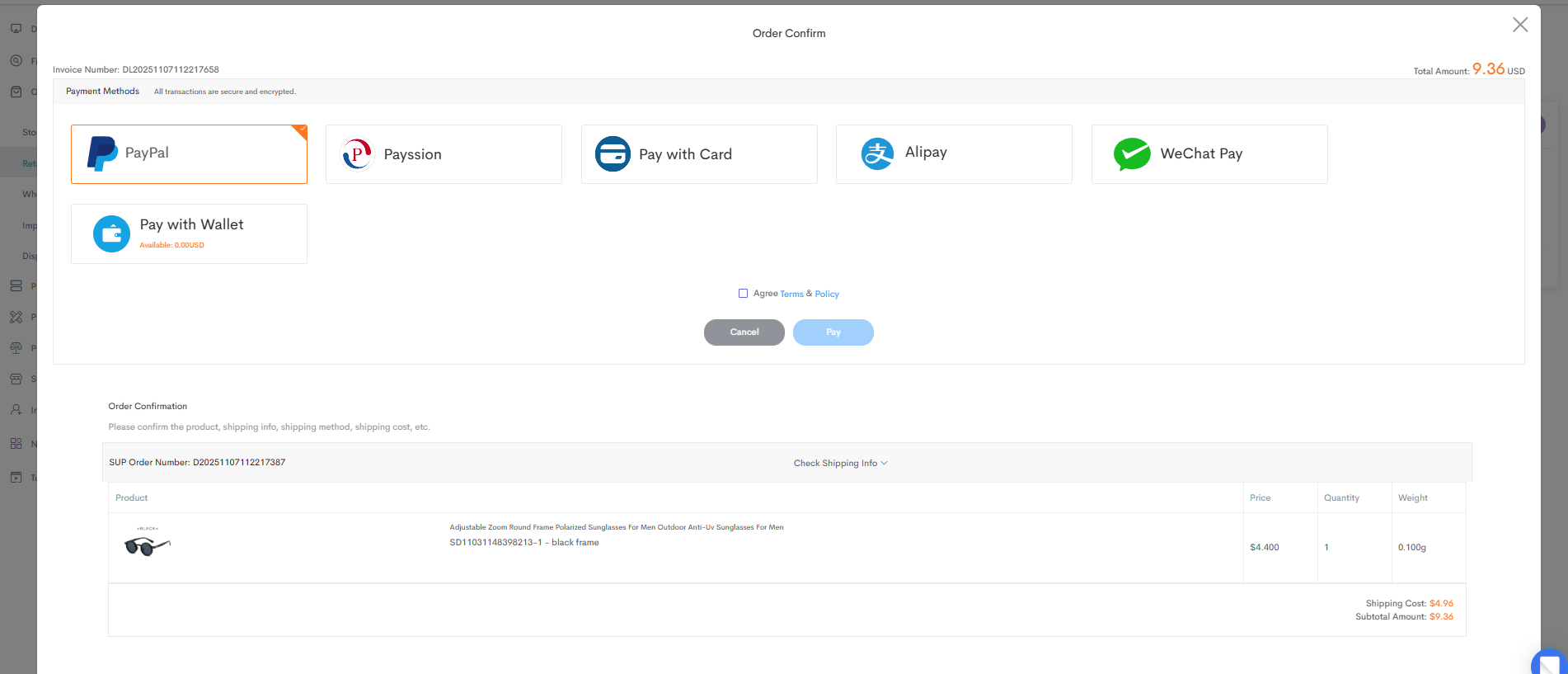

1. Customer places order and enters payment details

The process begins when the customer reaches checkout. They choose how they want to pay and enter their payment details. This might be card information, a digital wallet confirmation, or a login to online banking.

2. Payment gateway and processor verify the payment

After the customer submits the payment, the payment gateway encrypts the data. Think of it as a secure tunnel that protects the information while it moves online.

The payment processor then talks to the customer’s bank or card company. It checks if the card is real, if there’s enough money, and if the transaction is safe. If everything is okay, the payment is approved. If something is wrong, the payment is declined.

3. Payment approval and order confirmation

When the bank approves the payment, your store gets a confirmation. The customer sees “Payment Successful” or “Order Confirmed.”

At this stage, the money is authorized, which means it’s reserved but hasn’t fully moved to your account yet. The customer feels like the payment is done, but the system is still processing the money in the background.

4. Funds arrive in merchant account

Once the payment is authorized, the money goes into your merchant account, a special account for online payments. After a few days, it moves from the merchant account into your normal business bank account, ready for use.

Ecommerce Payment Methods and Options

In ecommerce payments today, mobile wallets and credit/debit cards are the two most commonly used methods.

According to a 2024 global payment report, mobile wallets made up 53% of online payment transactions worldwide. Credit cards ranked second at 20%.

But there’s more than just these two. Other growing options include Buy Now, Pay Later, and bank transfers or local payment methods, depending on the region.

بطاقات الائتمان والخصم

Credit and debit cards are the most familiar payment option for most online shoppers.

Customers simply enter their card details at checkout, click pay, and the payment is processed instantly.

- Credit cards work by letting the customer borrow against their credit limit and pay later.

- Debit cards directly deduct the amount from the customer’s bank balance.

For merchants, card payments run through a payment processor, and the funds eventually settle in your merchant account.

Networks like Visa, Mastercard, and American Express are well-known and trusted, which is why customers feel comfortable using them.

One thing to note: processing fees vary depending on the card network and the customer’s bank.

Digital wallets

Digital wallets have grown quickly because they make checkout faster and safer.

Wallets like Apple Pay, Google Pay, and باي بال let customers complete payment with just a tap or a face/fingerprint scan. No manual typing. No card number exposure.

Digital wallets also use tokenization, meaning the real card number isn’t shared during the transaction, which adds a layer of security.

They’re especially effective if your audience shops on mobile or belongs to younger demographics who prefer convenience first.

Buy now, pay later

Buy Now, Pay Later lets customers get the product now but split the payment into interest-free installments.

Services like Klarna, Afterpay, and Affirm are common examples you’ll see at checkout.

For merchants, the main benefit is simple: you still get paid upfront (or within the normal payout window). The BNPL provider takes on the responsibility of collecting the installments, and absorbs the credit risk, not you.

This is why BNPL often leads to higher conversion rates, especially for products with a higher price tag.

التحويل المصرفي

Bank transfers are another common ecommerce payment option. The customer logs into their bank app and manually sends the payment to the merchant. It’s straightforward and familiar for many buyers, particularly in B2B transactions where the order value is higher.

Compared to credit cards, bank transfers usually come with lower transaction fees, which makes them cost-effective for businesses. But they’re not instant. Processing can take a couple of days, depending on the bank and the region.

الدفع عند الاستلام

الدفع عند الاستلام (COD) allows customers to pay only after receiving their order, rather than upfront. This payment method is especially common in regions where credit card adoption is low or shoppers are wary of online payments.

COD can help build trust with customers who may hesitate to pay in advance, making them more likely to complete a purchase. On the flip side, it carries risks for merchants: if a buyer refuses the delivered item or refuses to pay, the seller can face financial losses and logistical challenges.

How to Choose the Right Ecommerce Payment Processor

If you run your own online store, choosing a payment processor is a decision worth thinking through carefully. Here are five key factors to consider when selecting the right ecommerce payment processor:

Compare costs and fees

Payment processors usually charge fees in three main ways: setup costs, monthly subscription fees, and transaction fees.

- Setup costs are one-time fees to get your account started.

- Monthly fees cover ongoing access to the platform and support.

- رسوم التحويل are a percentage of each sale or a fixed amount per transaction.

Knowing these costs upfront helps you avoid surprises and ensures your choice fits your store’s size and sales volume. Some providers are better for small stores with low sales, while others scale efficiently for high-volume or global sellers.

Make sure customers can pay anywhere, any way

Not every customer pays the same way. Some use credit cards. Many people prefer digital wallets like Apple Pay, تسوق الدفع or PayPal. In some regions, local payment methods are even more common than cards.

So the processor you choose needs to support the payment methods your customers already feel comfortable with. Studies show that around 10% of online carts are abandoned simply because the preferred payment option isn’t available. Not price. Not shipping. Just payment choice.

Payment preferences also vary by region. In the Asia-Pacific, nearly 70% of ecommerce payments are completed through digital wallets. But in Latin America and the US, wallets account for only about 20%.

That’s why, when choosing a payment processor, it’s not enough to just check fees. You also need to ensure that it supports the payment methods your customers actually use and can process payments in the countries and currencies you sell to. Miss either, and you risk losing sales before your customer even clicks “Place Order.”

Keep Payments Safe

When you accept payments online, keeping customer data safe isn’t optional; it’s part of building trust. In fact, most customers consider security one of the top factors when deciding whether to complete a purchase.

The first step is making sure your website connection is encrypted. This is where an SSL certificate comes in. It creates a secure link between your site and the customer’s browser so that any payment details they enter are scrambled and unreadable to outsiders.

Next, your payment processor should help you stay PCI compliant. PCI DSS is a security standard that applies to everyone who handles credit and debit card transactions. It’s basically a rulebook to make sure card data is stored and transmitted safely.

In short, pick a payment processor that handles encryption, PCI compliance, and fraud detection automatically. It saves you work, reduces risk, and helps keep customer trust intact.

Integration and Ease of Setup

Integration and ease of setup are key factors to consider. Look for a provider that works smoothly with your ecommerce platform, whether it’s شوبيفي, ووكومرس, BigCommerce, or a custom site.

Customer Support and Dispute Handling

Even with a solid payment processor, issues can happen, like failed transactions, chargebacks, or customer complaints. That’s why responsive customer support and clear dispute handling are essential.

A good provider offers multiple support channels (chat, email, phone) and clear procedures for resolving problems quickly. This helps you minimize downtime, prevent financial losses, and keep customers happy.

5 Top Ecommerce Payment Providers

With so many options available, choosing the right ecommerce payment provider can be overwhelming. Here are five popular platforms to help you make an informed decision:

باي بال

PayPal is one of the most recognized and trusted payment providers worldwide. As of October 2025, it held a 44% share of the ecommerce payment market, showing its continued popularity. Setting up PayPal is quick, and most customers are familiar with it, which can boost conversions. The main downside is higher transaction fees compared to some alternatives.

شريط

Stripe is known for its developer-friendly platform and flexible integration. It supports a wide range of payment methods, including credit/debit cards, digital wallets, and even Buy Now, Pay Later options. Stripe is great for growing stores or global sellers because it handles multi-currency payments and has robust fraud detection tools.

Square

Square is popular for businesses that sell both online and offline. It offers a simple setup, supports multiple payment methods, and integrates well with ecommerce platforms. Its strength lies in omnichannel selling, making it easy for merchants to manage both in-store and online payments in one place.

شوبيفاي الدفع

If your store is on Shopify, Shopify المدفوعات is a seamless choice. It’s built directly into the platform. The biggest advantage is simplicity, and in many cases, you avoid additional transaction fees. It supports major credit cards as well as Apple Pay and Google Pay. The limitation is that Shopify Payments is only available for Shopify stores and in certain countries.

كلارنا

Klarna specializes in Buy Now, Pay Later (BNPL) solutions, allowing customers to pay in interest-free installments. This option can increase conversion rates, especially for higher-priced items, while the BNPL provider takes on the risk of collecting payments from customers. It’s a popular choice for merchants looking to offer flexible payment options.

Ecommerce Payments FAQs

1. How to set up your ecommerce payment system?

First, choose an ecommerce platform or website builder. Then pick a payment provider like PayPal, Stripe, or Shopify Payments. Connect your store to the provider, add clear checkout buttons, and test a few orders to make sure everything works. Keep the steps simple so customers can pay without confusion or extra clicks.

2. What’s the difference between a payment gateway and a payment processor?

A payment gateway collects and passes the customer’s payment information from your checkout page. A payment processor works behind the scenes to talk to the bank and move the money. Some companies, like Stripe and PayPal, offer both. So you do not always need to choose two separate tools.

3. Do I need to worry about PCI compliance?

Yes, if your store accepts credit cards, PCI compliance matters. It means protecting customer card information from being stolen. The good news is most payment providers handle most of the security requirements for you. Just make sure you use a trusted provider and keep your site updated to stay safe.

افكار اخيرة

Getting ecommerce payments right isn’t only about processing transactions. It shapes how customers feel about your store. A smooth, secure checkout builds trust, reduces cart abandonment, and makes shoppers more likely to return.

When choosing a payment provider, keep things simple: look for clear fees, strong security, and a checkout experience that doesn’t slow people down. Even small improvements here can lead to noticeable results in conversions and sales.

And if you’re running an online store and want fewer operational headaches, Sup Dropshipping can help with sourcing, fulfillment, and shipping. That way, you can stay focused on what actually grows your business: products, marketing, and customers. Feel free to اتصل بنا if you ever need help.

عن المؤلف

يمكن

ماي هي مدوّنة في Sup Dropshipping وتتمتع بخبرة تزيد عن 5 سنوات في مجال التجارة الإلكترونية. إن شغف ماي بالتجارة الإلكترونية يدفعها إلى البقاء على اطلاع بأحدث الاتجاهات ومشاركة خبراتها معك من خلال مدونتها. تحب في أوقات فراغها قراءة رواية أو الدردشة مع الأصدقاء.

اترك تعليقاً